Posted on by Comments Off on Your Support Options with CPA Canada PEP and CFE

CPA Canada exams are grueling and require hours of dedicated study and practice. At some point, you may feel that you need supplemental support. Here are your options.

Option #1: One-on-one CPA tutor

You can hire a CPA tutor to sit down with you, act as your coach and provide one-on-one help. Tutors usually don’t have supplemental cases, they use CPA Canada’s cases and answer your questions. You pay per hour and the usual fees are $60-$100/hr (depending on experience).

Option #2: Case marking

You can hire someone mark your cases and pinpoint the areas to work on. The difference with this option is that you don’t have live sessions with someone, the feedback is done on paper, similar to CPA facilitators. You pay per marked case and the fee is usually $40-$100 (depending on case length).

Option #3: Supplemental cases, practice drills

You can get supplementary materials such as extra cases, drills, study notes. With this option, you would study independently using the materials. The prices vary greatly depending on the type of material you purchase.

Option #4: Coaching program

You can sign up for a coaching program. The great thing about a CPA coaching program is that it’s an amalgamation of above support sources: You receive the live coaching, supplementary materials, and case marking.

Which one is best for you? It depends on your circumstances and your budget. If you failed your exam twice, I highly recommend hiring a one-on-one tutor or signing up for a coaching program. These resources will help you find where you’re going wrong and help you correct and improve it. If you are taking your module for the first time, you may want to purchase supplemental materials and study independently. After a few weeks, if you feel that you’re struggling, consider upgrading to the other options.

Posted on by Comments Off on How to Download Survival Guides for CPA Canada PEP Modules

Update: The Survival Guides have been replaced by PEP Syllabus. Please seethis updated post.

The CPA Canada Survival Guides are an excellent resource to keep track of eBook readings, assignments, deadlines and deliverables. It’s a good idea to download and print them before your module starts, so that you complete your readings in advance.

Here are the steps to download the survival guide for any module:

Posted on by Comments Off on 5 Reasons Why Candidates Fail CPA Canada PEP and CFE Exams

When it comes to the CPA Canada PEP exams and Common Final Exam (CFE), there are specific reasons why some candidates struggle to pass. For some, it’s not knowing how to study for the exam. For others, it’s weak technicals. For majority, it’s running out of time and not being able to answer all the AOs .

Here are the top five reasons why candidates are unsuccessful at CPA exams and how to avoid these pitfalls:

1. Weak technicals

Without strong technicals, you are not going to reach depth in AOs, resulting in insufficient marks for passing. Here are few strategies that I’ve seen candidates take towards studying the technicals:

Full technical review strategy: Some candidates read everything, trying to cram as much technical knowledge as possible. This often results in burnouts and forgetfulness.

Minimal technical review strategy: Some candidates find technical too difficult to study, so they skip the complex ones and study basics. This results in getting NA/NC in complex topics which come up on exams often.

You should aims for the the middle:

Study some technicals, write more cases: Instead of fully reviewing all technicals, it’s better to study the most commonly tested topics, then focus your time on case writing. By continually applying technicals to cases and adding to your knowledgebase as you debrief, you refine your knowledge and achieve technical mastery.

2. Suboptimal study plan

PEP program takes 1.5-2 years to complete for most and CFE time off is usually 4-8 weeks. It’s important to develop an effective study schedule that fits into your everyday schedule during these times.

I suggest planning day-by-day what you’re going to do:

It’s important to plan early because there are many distractions in our daily lives, with balancing work, personal life, and other commitments.

If you’re a morning person: Wake up early, study for a few hours, head to work, and study as much as you can in the evening before going to bed.

If you’re a night owl: Get good sleep, head to work, and do most of your studies in the evening.

3. Poor case writing skills

Case writing is an umbrella topic that includes several skills, including formatting, outlining, time management, and hitting depth. CPA Canada PEP and CFE exams are unique in the sense that no other CPA designation around the world uses simulations (cases) to evaluate candidates. Cases prove to be challenging for candidates who are not native English speakers, fast typers, fast readers or who find it difficult to structure their thoughts under time pressure.

Here are the top 3 “must have” skills:

Stay organized: CPA cases are like puzzles. They throw different case facts and your job is to find and organize them, and solve the puzzle. When reading the case, put each piece in the right box. Use the BURN acronym to organize the key case facts: business information, users, requireds and necessary case facts.

Work on your typing speed: In my CPA Honour Roll student interviews, I ask top writers what is their typing speed. Most are above average, around 70-80 words per minute (WPM). if your WPM is less than 45, you need to work on that.

Write efficiently: CPA Canada solutions are not helpful. They are above-perfect answers that are unrealistic for candidates to write under exam conditions. You can use them to learn technicals, but you need “realistic solutions” to learn how to efficiently write cases. My PEP and CFE Review courses offer realistic solutions to several cases, that are actually manageable to write in the time limit.

4. Not understanding the CPA exams

Another common pitfall by candidates is that they don’t do enough research on how the PEP and CFE exams are marked and what specific concepts will be tested. If you are taking Core 1, or you’re an international trained accountant (ITA) challenging the CFE, you’ll find the CPA PEP and CFE blueprints confusing.

Research: Take the time to research on Google and YouTube for CPA exam blueprints and how each exam is tested.

Study resources: Use your study materials wisely and focus on few resources that add most value to your studies.

5. Mental unpreparedness

For some candidates, their internal emotions and their motivation gets in the way of their own success. There is lots of pressure on you, from co-workers, family, friends, and relatives. It seems that failing the CPA exam will disappoint everyone. However, fear stops your from focusing and thinking clearly. You have to stop fear and intimidation from getting the best of you.

Take time out, breath and relax. Remember that other writers are feeling as stressed and pressured as you. It’s important that you find a study partner or a study group that will positively influence you and give you an extra boost of motivation. You can find a study partner by joining my CPA Canada Facebook and WhatsApp groups. It’s also helpful to schedule time off in your schedule for relaxation and rest.

If you have failed you CPA PEP or CFE exams attempting on your own or with another CPA coaching provider, now is the time to consider a change. Gevorg, CPA has strategies, study materials and markers that will help you study smarter, find answers quicker and get results. I have overall 90% pass rate across our courses and we provide personalized coaching that will help to focus your studies.

Sign up for PEP and CFE Reviewprograms to learn the path to CPA success.

Posted on by Comments Off on What’s different about Gevorg, CPA CFE coaching program?

I offer a personalized CFE coaching program based on Honour Roll strategies. My candidates achieve overall 90%+ pass rate on the CFE. Here is a quick comparison:

Features

Gevorg, CPA CFE course

Other providers

Case marking

Access until you pass

100% Canadian owned

Day 1 case marking*

Flexible marking schedule

Weekly live coaching sessions*

Free access to CPA SpeedType™ time management and case typing training tool

*Some but not all CFE coaching providers offer Day 1 marking and weekly live sessions. Some providers offer 1-on-1 coaching through mentors or instructors who may not be subject-matter experts. T2202 certification is not issued by all providers. The information in this table is based on the information made available on competitor websites.

Student Reviews and Testimonials

Student reviews and testimonials of my CPA courses are available at Reviews page.

Course preview and details

You can watch free lessons and learn more by clicking on the cover image below. You can also get in touch with me for a quick consultation call.

When logging in for the first time, your user ID and password will be your 7-digit CPA ID number beginning with 4. Your password will be your email address. You will be requested to change your password when entering.

If you are unsuccessful, here are the next steps and answers to frequently asked questions.

Why was I unsuccessful?

There are different reasons. You may have struggled with technicals, time management, or efficient case writing. The first step is to look at your detailed transcript to see what Level you failed.

For Days 2/3:

Level 1 sufficiency: This is driven by both Days 2 and 3, with more emphasis on Day 3. Failing Level 1 means you didn’t achieve C and RC enough in your cases.

Decile ranking: Decile ranking is for Level 1 only. It shows how close you were from passing. For example, decile 1-3 means you were close to passing, while decile 8-10 means you were far. If you passed Level 1, you will not see decile ranking. Decile ranking is not available for Level 2, 3, or 4, nor Day 1 of the CFE.

Level 2 depth in FR/MA: This is driven by both Days 2 and 3, with more emphasis on Day 2. You didn’t achieve enough Cs in FR or MA.

Level 3 depth in role: This is driven by Day 2 only. You didn’t achieve enough Cs in your role (PM, Assurance, Finance or Tax).

Level 4 breadth: This is driven by both Days 2 and 3, with more emphasis on Day 3. You didn’t achieve enough Cs or RC in all competencies (for example, you may have scored NC in all Tax or Finance AOs).

For Day 1:

You will see only pass/fail assessment with no details in the transcript.

You will also receive a free Automatic Feedback Report (AFR). This report will tell you why you didn’t pass. It’s going to be uploaded to the same portal where you download the transcript (Certification Portal), 2 weeks after results date. You should download and review it. This report is free.

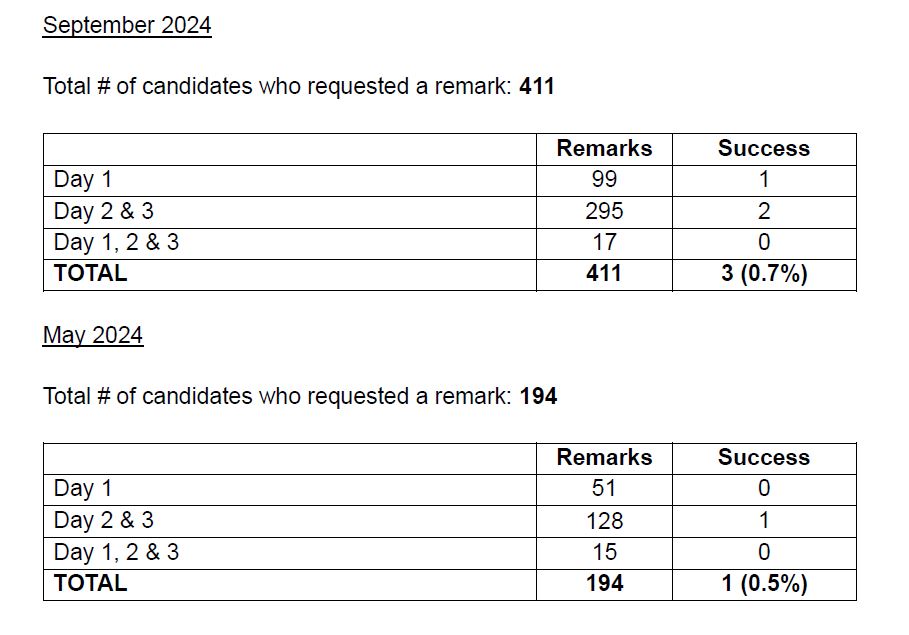

Should I ask for re-mark (appeal)?

No, I don’t recommend asking for re-mark. The chances of success are less than 1%. Below is a screenshot from September 2024 and May 2024 re-mark results released by CPA Canada:

Should I get a PAR report?

PAR provides a breakdown of each case, with comments on your performance. It takes several months to receive the PAR report and it is costly. I wrote a detailed post and description of anexample PAR here, please check it out.

Is the next CFE in May 2026 or June 2026?

The next CFE will be held June 2 to June 4, 2026. Usually CFEs are in May and September each year, but for 2026, the May 2026 CFE has been delayed to June, so it’s referred to as “June 2026 CFE“.

How many CFEs are left until the new 2027 CPA Professional Program (CPAPP)?

There are only 4 CFEs left:

June 2026 CFE

September 2026 CFE

September 2027 CFE

September 2028 CFE

Am I allowed to write immediately after in June 2026 CFE?

Yes, students who need to re-write the CFE don’t have to wait until next September, you can write CFEs back-to-back.

Should I write in June 2026 CFE or wait until September 2026?

It depends. The two big factors you should consider: (1) Learning a new Day 1 case, (2) Study time availability.

The Day 1 cases repeat annually, so your September 2025 Day 1 case will not appear in June 2026 CFE. This means you’ll need to learn a new Capstone 1 case. This is not a big problem because most Capstone 1 and Day 1 cases are similar in terms of formatting and AOs, you will learn it quickly.

The bigger question is whether you have time to study for June 2026 CFE. If you’re working in public practice, your employer may not let you take time off. If you’re working in the industry, you may have used up all your time off for the September 2025 exam.

Here’s my suggestion:

Talk with your employer and make sure you have time to study in spring 2026. You’ll need to take time off before the exam (3-4 weeks recommended). If your employer approves, write in June 2026, because your technical knowledge and case-writing skills are still fresh. Before registering, make sure to build a study plan and get proper support.

What Day 1 cases are in June 2026, September 2026, September 2027 and September 2028 CFE?

For the June 2026 CFE, the following Day 1 cases:

Karnat Bread Company Ltd. (KBC) v1

Viviana’s Trattoria Ltd. (VTL) v2

For the September 2026 CFE, the following Day 1 cases:

Singular Textiles Corporation (STC) v1

Meadowlark Entertainment Inc. (MEI) v2

There is no CFE in May 2027.

For the September 2027 CFE, the following Day 1 cases will be tested:

Singular Textiles Corporation (STC) v2

TBD, new case v1

For the September 2028 CFE, the following Day 1 cases will be tested:

TBD, prior case v2

TBD, new case v1

When should I start studying again?

This depends what CFE Days you are writing and which exam sitting you will be re-taking:

Re-writing in June 2026:

CFE Days 1,2,3 re-write: Start studying from November.

CFE Days 2, 3 re-write: Start studying from January.

CFE Day 1 re-write: Start studying from March

Re-writing in September 2026:

CFE Days 1,2,3 re-write: Start studying from Feb 2026.

CFE Days 2, 3 re-write: Start studying from March 2026.

CFE Day 1 re-write: Start studying from April 2026.

What should be my study plan as an experienced CFE writer?

Here is an effective plan to follow:

Step 1: Build a study plan. This shows weekly what activities to perform, what cases to write and what days to take off for personal errands.

Step 2: Review technicals, especially the areas you you didn’t do well based on the transcript.

Step 3: Re-do cases from your electives (especially if you didn’t clear Level 3).

Step 4: Write cases. If you’ve written all Capstone 2 (past CFE) cases, get supplemental CFE cases.

Step 5: Have your cases marked or self-mark them yourself.

Step 6: Get a study partner, study resources, or sign up for a coaching program.

Where can I get more study resources (tutoring, coaching, personalized support)?

There are several options available to you:

Tutors: CPA tutors provide 1-on-1 help by connecting with you virtually or meeting in-person. Their expertise varies and it’s important that you find a tutor that fits your needs. CPA Canada publishes a list of tutors which you can request by contacting your provincial CPA school. The tutoring fees are normally $60-$80 per hour.

Supplemental cases: Writing more cases will help to broaden your technical and improve your time management skills. You can obtain supplemental CFE caseshere. The price range is $60-$97.

Coaching programs: CPA exam coaching programs are more comprehensive than tutoring. They provide study notes, extra cases, marking services, and subject-matter experts work with you to understand your weaknesses and help you achieve better exam performance. Coaching program fees vary and it’s important that you find a program that’s effective.

What’s Gevorg and what’s different about your CFE coaching program?

Gevorg is a personalized CFE coaching program that’s based on Honour Roll strategies. Our candidates achieve overall 90%+ pass rate and several graduate with distinction. Here’s a quick comparison.

Features

Gevorg, CPA CFE course

Other providers

Case marking

Supplemental cases

100% Canadian owned*

Day 1 case marking*

Flexible marking schedule

Live coaching sessions*

Free access to CPA SpeedType™ time management and case typing training tool

*Some but not all CFE coaching providers offer Day 1 marking and live sessions. T2202 certification is not issued by all providers. Some providers are U.S. owned. The information in this table is based on the information made available on competitor websites.

What does Gevorg CFE coaching program offer?

Our CFE coaching program that teaches technicals, case writing skills and proven strategies towards the CFE. The CFE Reviewprovides the following learning materials:

New CFE practice cases with solutions and feedback guides

Dedicated Day 1 prep course with marking

Marking of two (2) Day 1, one (1) Day 2 and three (3) Day 3 case (total of 6 cases marked)

Weekly live tutoring sessions

Case writing walkthroughs

Case outlining templates

Quantitative analysis templates

Time management methods

Memory aids

Technical study notes

8-hours of engaging video lessons

Historical CFE data

Supplemental practice drills (including DAIS)

Study plan for the CFE

Case checklist

Technical review checklist

You’ll also get one-on-one coaching with a tutor. You get access to the course materials immediately and you keep access until you pass, no matter how long it takes.

Do you mark extra cases?

Yes, our CFE program includes 6 case marking and we can mark extra cases if needed.

Conclusion

I know failing the CFE is demotivating. It doesn’t mean you’re not smart or unable to succeed, it means you need a new strategy. Take some time think about your options and decide what you will do differently next time. If you feel CFE Review is the right coaching program for you, you can watch preview lessons here.

Posted on by Comments Off on Here’s a List of All Special Reports for CPA Canada PEP and CFE Exams

Special engagements or special reports are a common AO in the CPA Canada PEP exams and the Common Final Exam (CFE). Candidates are familiar with some of them, such as Attestation engagements to report on compliance (CSAE 3530) and Direct engagements to report on compliance (CSAE 3531), but you may face a new special report on the exam.

Here is a list of all possible special reports you may get, per the CPA Canada Competency Map:

Assurance engagements related to F/S: • An audit of general-purpose financial statements (CAS 200, 220, 250, 720) • An audit of financial statements prepared in accordance with special-purpose frameworks (CAS 800) • An audit of single financial statements and specific elements of a financial statement (CAS 805) • An engagement to report on summary financial statements (CAS 810) Other assurance engagements: • Reporting on controls at a service organization (CSAE 3416) • Assurance on other matters (i.e., not financial statements or financial information) (5021) • An audit of internal controls over financial reporting that is integrated with an audit of financial statements (5925)

Review engagements: • Engagements to review historical financial statements (CSRE 2400) • Auditor review of interim financial statements (7060)

Other engagements: • Attestation engagements other than audits or reviews of historical financial statements (CSAE 3000) • Direct engagements (CSAE 3001) • Attestation engagements to report on compliance (CSAE 3530) • Direct engagements to report on compliance (CSAE 3531) • Compilation engagements (9200, AUG 5) • Compilation of a financial forecast or projection (AUG 16) • Reports on the results of applying specified auditing procedures to financial information other than financial statements (CSRS 4400. Note: was called Section 9100 but archived now.) • Agreed-upon procedures regarding internal control over financial reporting (9110) • Reports on application of accounting principles (7600) • Auditor’s involvement with offering documents, including assistance to underwriters and others, consent to use of report, etc. (7150, 7170, 7200, AUG 6) • Reports on supplementary matters arising from an audit or review engagement (CSRS 4460)

Where can I get study resources for these?

These are discussed mostly in the CPA Canada’s Learning eBook. The eBook’s Assurance chapters cover: CAS 800, 805, 810, CSRE 2400, CSAE 3416, 3530/3531/ 3000/3001.

EBook is a good resource, but it’s not perfect. If you would like more coverage of special reports, with templates and explanations, check out my CAS Notes and the Assurance course.

Need help passing CPA exams?

Sign up for Assurance Review and CFE Reviewprograms to get case marking, extra practice cases, study plan, engaging video lessons and personalized coaching with me.

Posted on by Comments Off on How to Write Quantitative and Qualitative Analysis in CFE Day 1, Day 2 and Day 3 Cases of CPA Canada

In this article, I’ll discuss how to approach quantitative (quant) and qualitative (qual) analysis per each of the CPA Canada Common Final Exam (CFE) Days:

CFE Day 1

You’ll face Strategic (ST) and Operational (Op) issues.

For ST, you’re required to analyze quantitatively and qualitatively. Follow the steps below for quants:

Start with excel: write appendix title, purpose, conclusion

Choose the right “technique” (ie, tool for the job). Eg, if it’s valuation, choose between asset-based, transaction-based and market-based (multiples). Use case facts to determine the right technique (eg, if “capitalization rate” given, then it’s transaction-based CCF valuation technique).

Apply the template (horizontal, vertical, top-down, etc. I provide templates in my CFE Review course)

Show support for calculations

Summarize the analysis in the memo

Write 2-3 assumptions in the memo

Follow the steps below for qual:

Use Word, format in bullet list

Write 4-5 Pros and 4-5 Cons

Write a balanced analysis, including both pros and cons

Integrate AT LEAST 4-5 situational analysis factors in EACH issue

For OP, the requirds are mostly qual-based. They have to do with minor issues, eg board issues, performance issues, ethical issues and so on. You still need to integrate 4-5 times overall in the operational issues. The format varies based on the type of issue. To get good at OP issues, practice with sample cases and debrief from the solutions.

CFE Day 2

The quants come into play at MA requireds. Follow the same approach as with Day 1, but this time go into more depth in your analysis. If there are uncertainties, perform sensitivity analysis. If there are multiple scenarios, address all of them. It’s easy to lose track of time with MA quants, so it’s important that you budget your time and move on when the time is up. Passing Days 2/3 Level 2 requires depth in FR or MA, so if you focus on getting Cs in FR, you’ll pass with RCs on MA.

There is no qual in Day 2 unless you are taking Finance, PM or Tax. See below for discussion on how to address these.

CFE Day 3

The quants can be tested as part of MA, Finance, S&G or Tax. The challenge with Day 3 is time, so the goal is to write a quick analysis in Excel and summarize in the memo. Don’t write assumptions, don’t write detailed explanations nor detailed conclusions. You’ll have about 7-10 minutes to do the quants, so move quickly. Getting RC in all quants in Day 3 is enough to pass the CFE Days 2/3.

The qual can be tested as part of Finance, S&G or Tax. There can be different requireds but generally “pro/con” format is applied to S&G, “bullet list” format is applied to Tax, and “bullet list/table” format is applied to Finance. For example, if the Fiannce AO asks you to discuss the financing sources, create a table with 3 columns: financing source, pros, and cons, and discuss in each row each of the options (eg. see TinyCo case from CFE 2019 Day 3). More detailed examples are available in my CFE Review course.

Need help passing CPA CFE exam?

Sign up for theCFE Reviewprograms to get case marking, extra practice cases, study plan, engaging video lessons and personalized coaching with me.

Posted on by Comments Off on Tough AOs! How to Handle Complex Topics in CPA Canada PEP and CFE Cases

A best practice with writing CPA Canada PEP and CFE practice cases is to put a timer and practice under the exam setting. In doing so, you develop time management skills and improve your case writing.

During this process, you’ll often run into situations where you can’t answer all technicals. Even though you identify the right required, you don’t know how to actually answer it.

What to do when you don’t know an AO?

Some students pause their timer, look up the relevant technical notes, and then resume the timer and answer the required. If you do this, you are not exactly imitating the exam setting.

Other students leave that required totally blank and mark it for debrief at a later point. With this approach, you’re not challenging yourself and again not imitating the exam setting.

Best approach

I know it’s temping to check your notes or the solution and work backwards. This is a bad idea. You are better off doing it under exam conditions and getting poor results, as opposed to taking the easier route. When you come across a situation where you don’t know the technical, keep the timer going and try to answer your best by referring to the Handbook (don’t look at your notes/solution).

Don’t leave it totally blank, attempt it, take a guess if you need to, you’ll be surprised how often you are on the right track. When debriefing, mark these AOs for re-attempt and study the technical during debrief.

The reality is that during PEP and CFE exams, you’ll very often come across AOs that are totally new and you’ll be stumped. You have to develop the skill on addressing unknown technicals. The strategy is to:

Budget a reasonable time

Look up the technical in HB/CAS/ITA (if applicable)

Apply relevant case facts

Tie to user preferences

Recommend

This will often give you RC, which is magnitudes better than NA.

Need help passing CPA exams?

Sign up for theCore 1 Reviewand CFE Reviewprograms to get extra practice cases, study plan, engaging video lessons and personalized coaching with me.

Posted on by Comments Off on Writing CPA Canada Practical Experience Requirements (PERT) – Technicals

I often receive a question from a CPA candidate in the EVR route on how to write the technical section of the PERT.

Here are general guidelines:

Write experience for Financial Reporting (FR), Management Accounting (MA), and Finance (skip Assurance and Tax unless you’re in public practice)

Write 2-3 examples for each sub-competency

Make each example at least 1/2 page long (in Word)

Follow CARL format (challenge, action, result, lesson learned)

Think of it like writing a case: What is the issue? How did you analyze it? What’s the recommendation?

Have titles for each section and give lots of details.

7 Tips to write the PER report

Get CPA PER Coaching

I’m excited to release Canada’s first PER coaching program with dozens of Level 2 examples, templates, video lessons, marking services, and more. Check out sample free lessons at PER Review.

Posted on by Comments Off on How to Write Control Weaknesses (WIR) in CPA Canada PEP and CFE Cases

Control weaknesses are a common assessment opportunity (AO) in CPA Canada’s PEP program, starting from Core 1 and leading all the way up to the Common Final Exam (CFE). It is something you should know well, even if you’re not taking Assurance as your elective.

Candidates often face the trouble of identifying the control weakness issue and understanding how to analyze it properly. Here’s a step-by-step guide:

Step 1: Find the required.

The case will give clear indications that you have to discuss the weaknesses. For example, here are requireds from past CFE Day 3 cases:

(1) CFE 2020 Jump Inc:

(2) CFE 2018 Perkins Packing Inc.:

(3) CFE 2015 Katwill Lodge Inc.:

The above examples have the trigger words “control weakness” or “improvements to processes.”

Step 2: Determine the area.

The control weakness could be specific to the accounting controls (eg payable process), or IT system (eg new ERP). In both cases, your approach is the same (see the next step).

Step 3: Apply WIR template.

Apply the WIR (weakness, implication, recommendation) template.

Step 4: Write your analysis.

Read the relevant appendix in the case and write your analysis:

Weakness – what is wrong with the process? Look for 4-5 issues. For example: lack of segregation of duties, no approvals, cheques aren’t signed, lack of IT controls (eg passwords aren’t changed frequently), no disaster recovery plan. Every case will have different issues, find these specific issues in the appendix. For this part, write only 1 sentence, only the specific case fact.

Implication – how does it impact the company? Write how the users, operations, and financials are impacted. Make sure to answer the “so what” question to get depth (“C”). Write 2-3 sentences in this part.

Recommendation – what can the company do to fix the weakness? Write 1-2 actionable items, only 1-2 sentences in this part.

Step 5: Practice WIR and debrief.

Practice control weakness requireds until you get Cs. You can practice using CPA Canada cases and get extra mock exam cases for supplemental practice. Make sure to debrief the cases properly so that you learn lessons and don’t repeat the same mistakes.

Need help passing CPA exams?

Sign up for theCore 1 Reviewand CFE Reviewprograms to get extra practice cases, study plan, engaging video lessons and personalized coaching with me.